New IGD research warns convenience growth is lagging behind the wider grocery market as competition intensifies.

IGD (Institute of Grocery Distribution) forecasts that the global convenience channel will grow from around US$ 900 bn in 2025 to over $1 trillion in sales by 2030, with the world’s top 20 operators accounting for over US$ 80bn.

However, the insight provider also predicts the channel will lose share in the grocery market as it faces rising competition from discounters, supermarkets, and rapid delivery services.

IGD’s ‘Global convenience trends 2026’ report finds that while convenience will continue to grow at 3.5% CAGR to 2030, this will trail total grocery growth of 4.0% CAGR. As a result, IGD expects the channel’s share of grocery will fall from 10.7% in 2025 to 10.4% in 2030.

Sneha Haria, Insight Manager at IGD, said: “The headline growth masks a structural challenge: convenience risks becoming a bigger channel with a smaller role in grocery spending unless retailers and suppliers adapt. The channel’s historic advantages are being eroded, and without change, it will continue to lose share.”

Europe and Asia lead the pack

IGD’s analysis shows that convenience’s growth and market share will vary greatly by region.

North America, the largest convenience market globally, is expected to grow the slowest, with market share declining from 16.9% in 2025 to 15.1% in 2030 as discounters and rapid delivery intensify competition.

Europe is projected to deliver the strongest market share gains, rising from 11.3% to 11.9%, driven by aggressive estate expansion and franchising.

Asia will contribute the largest increase in absolute sales, but convenience penetration will remain below 8% as traditional retail and local food markets continue to compete strongly.

Why convenience is losing share

IGD’s research identifies several forces driving share decline. Discounters are expanding locally and attracting value‑conscious shoppers, while supermarkets are sharpening small format propositions and fast delivery platforms are reducing immediate‑need store visits.

Rising operating costs and regulation limiting pricing flexibility are also impacting performance, as is shoppers’ perception of convenience being an expensive channel, particularly during periods of high inflation.

Together, these factors are eroding convenience’s traditional advantages on proximity, speed and mission clarity.

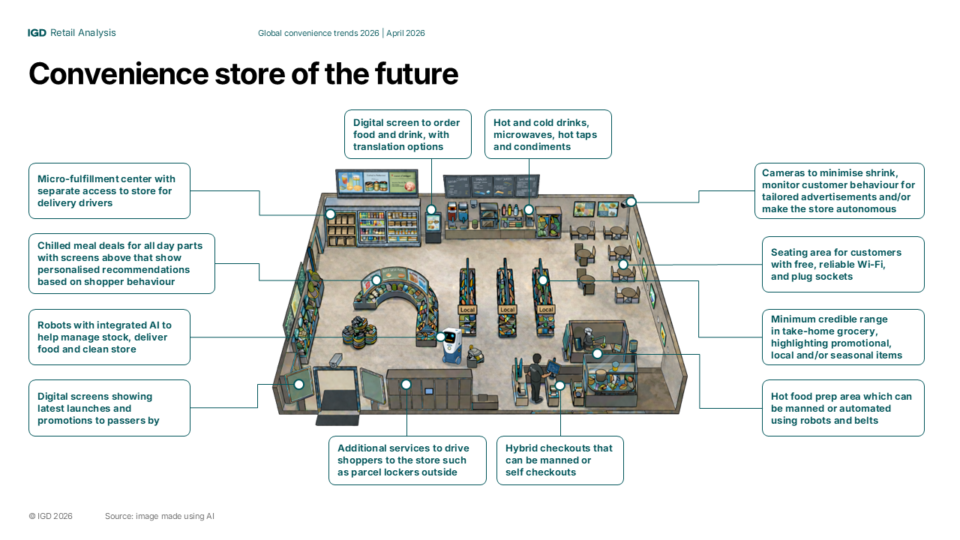

Choice over proximity

IGD’s analysis highlights that convenience operators gaining share are those redefining the role of the store, rather than relying on proximity alone.

Successful retailers are increasingly focused on:

- Creating clear food‑for‑now and food‑for‑later missions.

- Strengthening value credentials through private label, loyalty, and simpler pricing.

- Using automation and technology to protect margins and improve efficiency.

- Adding services, food, and experiences that competitors struggle to replicate locally.

Haria added: “Convenience can no longer rely on proximity to justify its place in grocery. The operators gaining share are deliberately reshaping their offer around clear food missions, visible value, and everyday usefulness.”